Leverage, Liquidation Price, and Forced Liquidation Mechanics

Leverage is the part of perpetual trading that rewards and punishes the fastest. This guide explains what leverage actually changes, how your liquidation price is set, why Hyperliquid uses mark price, and how to keep a safety buffer before you trade larger size.

What leverage actually changes

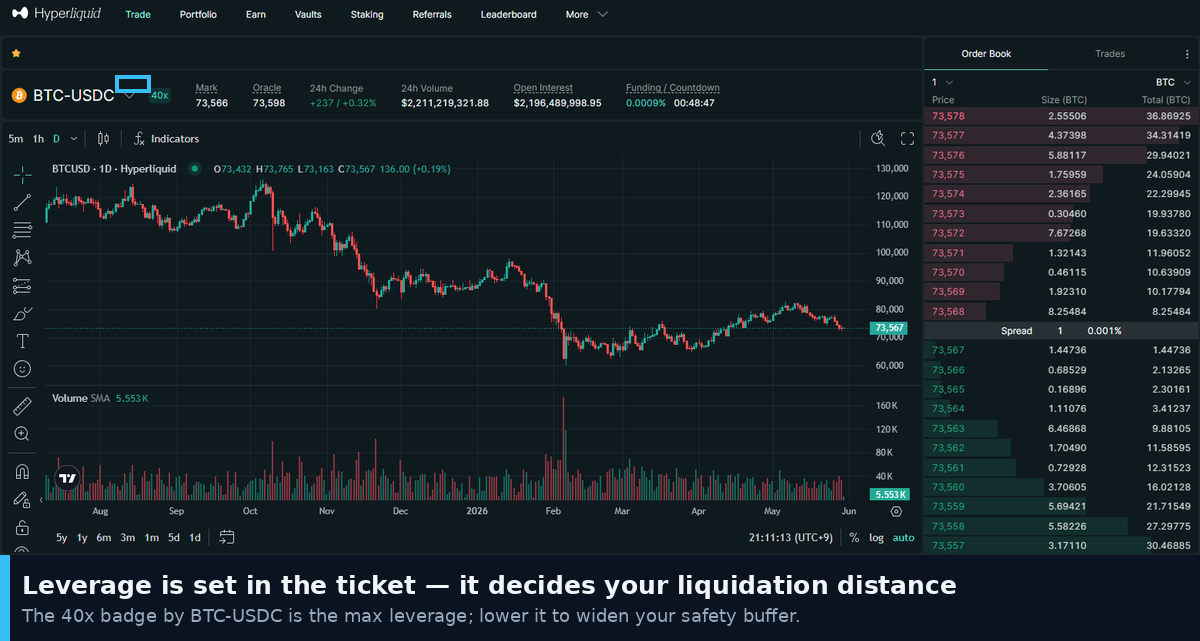

Leverage lets a smaller amount of margin control a larger position. On Hyperliquid you can set it from 1x up to a per-asset maximum, and that maximum depends on the asset. Higher is not better; it mainly decides how little room your trade has before trouble.

Think of leverage as your margin for error, not as a profit multiplier. A 2x position can absorb a much larger move against you than a 20x position built on the same idea. Same direction, very different survival distance.

Where liquidation risk comes from

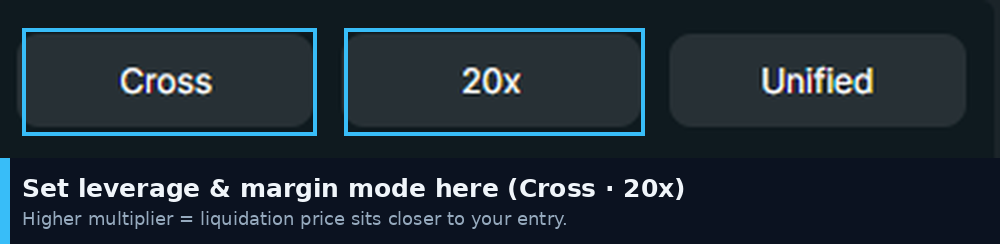

Liquidation happens when your positions move against you until your equity falls below the maintenance margin required to hold them. The margin that counts depends on your mode: with cross margin, your whole account value backs the position; with isolated margin, only the margin you assigned to that one position is at stake.

This is rule-based, not random, but it is not a guarantee of safety either. Markets can move quickly, and how much margin remains depends on execution and on the margin mode you chose.

Why Hyperliquid uses mark price, not the last trade

Liquidations on Hyperliquid are measured against the mark price, which combines external exchange prices with Hyperliquid's own order book rather than relying on a single last trade. The same mark price is used for margining, liquidations, take-profit and stop-loss triggers, and unrealized PnL.

For you, that means watching mark price and your liquidation price, not just the last number that printed on the chart. In volatile moments the last trade and the mark price can briefly diverge, and it is the mark price that decides your position.

What happens during a forced liquidation

When a position must be liquidated, Hyperliquid first tries to close it with market orders into the order book. If equity keeps falling past deeper thresholds and the book cannot absorb it, a backstop liquidation can occur through the liquidator vault. In plain terms: you can lose the margin allocated to the position, and it can happen before you have time to react.

How to keep a safety buffer

A few habits keep most beginners out of forced liquidations:

Use lower leverage while you are still learning.

Prefer isolated margin when you are testing a single position.

Do not add size just because PnL is green.

Decide where your stop goes before you enter.

Check that your liquidation price is not sitting inside normal daily volatility.

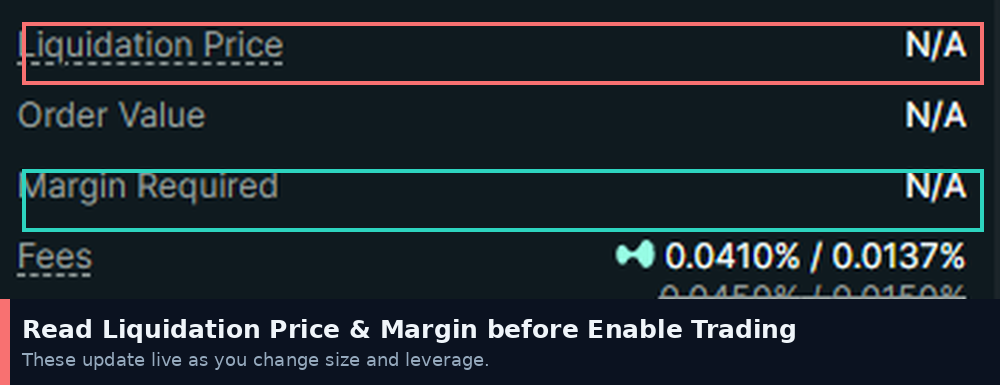

Before you confirm any order, read the live Liquidation Price and Margin Required shown under the ticket. If the liquidation price is uncomfortably close to the current price, lower your leverage until it is not.

Where to go next

Leverage and liquidation set the boundaries of a trade. The next thing to understand is funding, the hourly payment between longs and shorts that quietly adds to or subtracts from a position you hold.

Educational content. Not investment advice. Trading perpetual futures involves substantial risk, including the loss of your margin.

Further Reading

Hyperliquid in 6 Minutes: The Trader's Cheat Sheet from CEX to On-Chain Perps

If you can read a Binance order book, you can already trade on Hyperliquid — but the account underneath looks nothing like one. Here is what changes, and what to check first.

Leverage on Hyperliquid: How Far Are You From Liquidation, Really?

Higher leverage shortens your distance to liquidation. Here is how Cross and Isolated margin behave on Hyperliquid, what the margin ratio actually measures, and when to dial leverage back.

Market vs Limit Orders on Hyperliquid: Which One You Click First

Market orders execute instantly at the best available price. Limit orders give you exact price control and lower fees. Here is how to choose on Hyperliquid, with a beginner-safe default.